Open Enrollment has begun in Idaho and will begin in the other WWAMI states on November 1, however, between exams, clerkships, Step exams, and residency interviews, your insurance needs are probably the last thing on your mind. But as a medical student, making smart insurance choices now can save you money later. Depending on your specific needs and circumstances, you may or may not want or need to change your health insurance plan for 2025.

Reasons that Medical Students Change Insurance Plans

- Moving to a new state: Your current coverage might not work in your new location

- Aging out of parental coverage: Turning 26? You’ll need your own health insurance plan

- Developing new health needs: You may have different medical needs and your current plan may no longer be the best fit

- Preferred providers: Your desired providers providers may accept different insurance plans than what you currently have

- Changing Financial Priorities: Your insurance plan might have changed the price or coverage options for services/medications that you use. Or your own financial preferences may have changed and you want to shift to a different “tier” of coverage

- Getting married or divorced or having kids: Major life events can qualify you for special enrollment periods

If you are happy with your current plan, you may not think that you want to change your plan for 2025, however, everyone should review the 2025 coverage brochures for their respective health insurance plan. Health insurance companies change the prices and the coverage options every year, so services/prescriptions/providers that were covered this past year may not be covered next year.

Signs that It May Be Time to Switch

- You’re paying for services you never use

- Your preferred doctors aren’t in-network

- Prescriptions aren’t covered adequately

- Deductibles eat up too much of your budget

- You’re planning to travel for clerkships and need better coverage

Common Pitfalls to Avoid

- Don’t automatically renew without reviewing changes

- Don’t pick the cheapest plan without understanding coverage

- Don’t forget to factor in mental health services

- Don’t assume all university health center services are covered

- Don’t miss enrollment deadlines

Remember that financial aid can help cover health insurance costs like monthly premiums for comprehensive plans. Join a SOM Financial Aid Zoom Office Hours session to learn more about this process.

Licensed health insurance navigators or health insurance brokers can help you review the plan options and think through these types of questions when assessing your needs. Their services are free and we recommend scheduling an appointment with them early as their schedules will fill quickly.

Action Steps

- Review Your Current Plan

- List what you actually use vs. what you’re paying for

- Calculate your total yearly costs (premiums + deductibles + copays)

- Check if your medications and doctors are covered

- Research Alternatives

- Compare marketplace options, Medicaid plans, and university plans (where available)

- Check eligibility for Medicaid

- Schedule a free consultation with a health insurance navigator or broker

- Make the Switch

- Mark your enrollment deadlines

- Gather necessary documentation

- Ensure no coverage gaps during transition

The best insurance plan balances your health needs, budget, and peace of mind. Take time to evaluate your options and don’t hesitate to ask for help from licensed health insurance experts.

Here’s what we shared about Open Enrollment in the Oct. 3, 2024 newsletter:

Open Enrollment 101: Start thinking now about your gateway to health coverageAction Items:

2025 health insurance open enrollment is coming! This is the time when you can obtain health insurance for the 2025 calendar year. Each week, we’ll share information about various topics related to health insurance, how to prepare for open enrollment, things to consider when selecting a plan, and other topics.

MS2 students: because you will be starting clerkships in 2025 and will be moving in-and out-of-state, it is especially important to review your health insurance options. Many plans do not provide out-of-state coverage for routine care, so you should take action now to prepare for the upcoming clerkship cycle.

Note: By law, the UW School of Medicine cannot provide advice on health insurance plans. Students should contact certified health insurance professionals for advice.

What is Open Enrollment?

Open Enrollment is a specific period that occurs once a year during which individuals can enroll in or make changes to their health insurance plans for the upcoming calendar year. This period is crucial because it’s the only time when you can sign up for a new plan, switch plans, or make modifications to your existing coverage for the upcoming year without needing a qualifying life event (aka Special Enrollment Period).

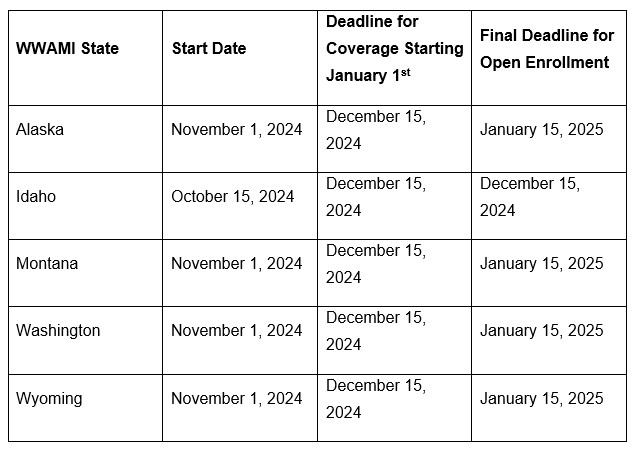

Key Dates

|

|

|

Note: For university-sponsored plans (not available in all WWAMI states), the timing can differ based on your university’s schedule. Not all WWAMI partner universities offer health insurance plans. WWAMI partner universities who do offer health insurance plans may have different open enrollment periods for their student health insurance plans, often coinciding with the end of the calendar year or the beginning of the academic and/or plan year.

|